The envelope arrives in your IRIS portal inbox with the Federal Board of Revenue letterhead. Or perhaps your accountant calls with the news: FBR has issued a notice against your business. Your stomach drops. What does it mean? What do you need to do? How much time do you have?

For most Pakistani taxpayers — individuals, freelancers, and business owners alike — an FBR tax notice feels like a crisis. In reality, most FBR notices are manageable and resolvable when handled correctly, promptly, and with proper documentation.

The critical word is correctly. Ignoring an FBR notice, submitting an inadequate response, or missing the reply deadline can transform a manageable query into a formal demand, a penalty, or a full tax audit. This guide gives you a complete, practical roadmap for handling FBR tax notices in Pakistan in 2026 — from understanding what type of notice you have received to submitting a compelling, documented response.

What Is an FBR Tax Notice in Pakistan?

An FBR tax notice is an official communication issued by the Federal Board of Revenue under the Income Tax Ordinance 2001 or the Sales Tax Act 1990, requiring a taxpayer to take a specific action — typically to provide information, clarify a discrepancy, pay a demand, or appear for an audit.

FBR issues notices through the IRIS portal (the primary digital channel), by post, and in some cases through field offices. Since FBR's digitization drive, most notices are now issued through IRIS with a barcoded reference number that can be verified online.

Notices are not automatically an accusation or a finding of wrongdoing. Many are routine — generated automatically by FBR's risk profiling system when data discrepancies appear, when a taxpayer has not filed a return, or when FBR wants to verify information declared in a return.

Understanding what type of notice you have received is the most important first step in responding appropriately.

Types of FBR Tax Notices in Pakistan

Different notices require different responses. Here are the most common categories:

Section 114(4) Notice — Non-Filing of Return: Issued to individuals or entities who were required to file an income tax return but did not. The standard response is to file the required return promptly.

Section 122(5A) Notice — Amendment of Assessment: FBR proposes to amend your already-filed assessment because they believe income was understated or a deduction was overclaimed. Requires a substantive documentary response.

Section 176(1) Notice — Call for Information: FBR asks you to provide specific information or documents — bank statements, contracts, invoice records — for verification purposes.

Section 177(1) Notice — Audit of Accounts: FBR selects your return for audit and requests full accounting records, financial statements, and supporting documentation for the declared tax year.

Section 111 Notice — Unexplained Income or Assets: FBR has identified assets or income in your wealth statement or financial records that cannot be explained by your declared income. One of the more serious notice types.

Section 137(2) Notice — Recovery of Tax: FBR demands payment of an assessed tax liability. This is a demand notice requiring either payment or a formal appeal against the assessment.

Section 214D Notice — Audit on Random Basis: Random audit selection notice. FBR has selected your return for scrutiny through their computerized balloting system.

Show Cause Notice (Section 182): Issued before FBR imposes a penalty, giving you the opportunity to explain why a penalty should not be levied.

Each notice type has its own response requirements, documentation needs, and deadline structure.

Why Responding to FBR Notices Correctly Matters in 2026

Pakistan's FBR has significantly enhanced its data analytics and cross-referencing capabilities. In 2026, FBR's systems automatically match declared income against banking data, utility connections, vehicle registrations, property transactions, and third-party withholding statements. Discrepancies generate automatic notices.

The volume of notices has increased substantially — but so has FBR's capacity to act on inadequate or non-existent responses.

Here is what happens when taxpayers handle notices incorrectly:

Ignoring a notice: FBR treats non-response as constructive admission of the issue raised. Ex-parte assessments are raised — meaning FBR issues an assessment against you without your input, typically at the maximum possible liability. Appeals become more difficult and expensive from this position.

Inadequate responses: Submitting a brief letter without supporting documentation is rarely sufficient. FBR officers reviewing responses are looking for documented, evidence-backed explanations. Vague or undocumented responses lead to escalated proceedings.

Missing deadlines: Each notice has a response deadline — typically 15 to 30 days from the date of notice. Missing the deadline eliminates your right to respond and allows FBR to proceed with enforcement action.

Incorrect understanding of notice type: Responding to a Section 177 audit notice as if it were a simple information request — without providing the full accounting records required — creates a non-compliance finding that carries its own penalties.

Correct, timely, and well-documented responses resolve the vast majority of FBR notices without escalation. The cases that escalate into formal disputes are almost always those where the initial response was inadequate or absent.

Key Principles for Handling FBR Tax Notices Effectively

Before diving into the step-by-step process, understand these core principles:

- Read carefully: Identify the specific section of the Income Tax Ordinance or Sales Tax Act under which the notice is issued — this determines what response is required

- Act promptly: Never wait until the deadline is imminent; start the response process immediately

- Document everything: Every claim made in your response must be supported by documentary evidence

- Be professional and factual: FBR notice responses are legal communications, not arguments; maintain a formal, factual tone

- Request extensions when genuinely needed: If the documentation gathering requires more time than the deadline allows, FBR allows extensions upon written application — but request this before the deadline expires, not after

- Keep copies: Retain copies of every notice received and every response submitted, with delivery confirmation

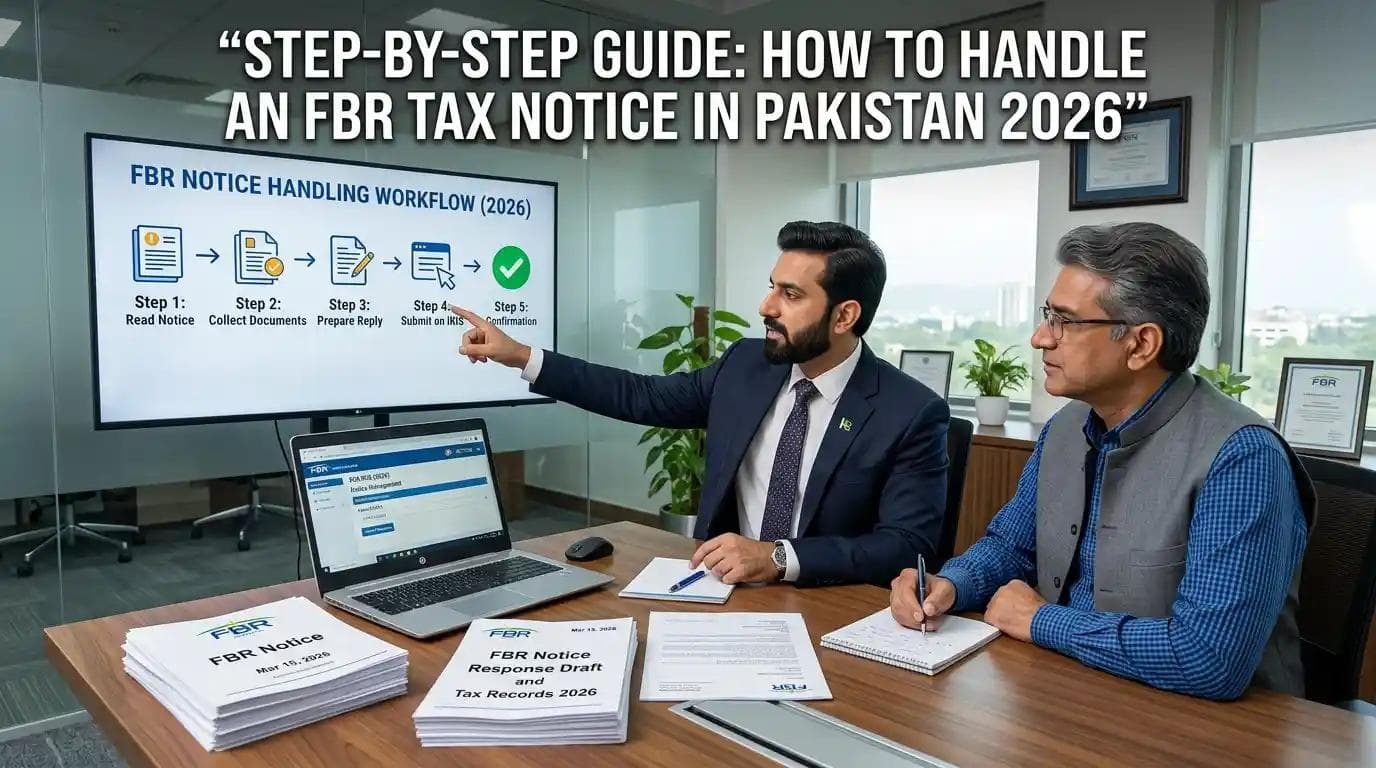

Step-by-Step Guide: How to Handle an FBR Tax Notice in Pakistan 2026

Step 1: Read the Notice Completely and Identify the Type

Do not panic — read the entire notice carefully. Identify:

- The section of the law under which it is issued

- The specific issue or query raised

- The information or documents requested

- The response deadline

- The designated officer and address for response

If the notice contains legal language you are not familiar with, seek professional help before proceeding.

Step 2: Verify the Notice's Authenticity

FBR notices should carry a barcoded reference number. Verify the notice's authenticity by logging into your IRIS portal at iris.fbr.gov.pk and checking your inbox and active cases. Fraudulent notices occasionally circulate — always verify through the official IRIS system before taking any action.

Step 3: Gather Your Financial and Business Records for the Relevant Period

Most FBR notices relate to a specific tax year. Pull together all records for that period:

- Filed income tax return with acknowledgment receipt

- Wealth statement for the year

- Bank statements for all personal and business accounts

- Withholding certificates received from clients or employers

- Sales invoices issued and purchase invoices received

- Financial statements (profit and loss, balance sheet) if applicable

- Contracts, agreements, or correspondence related to the queried transactions

- Property documents, vehicle registration records (if these are referenced in the notice)

The strength of your response depends entirely on the quality and completeness of your documentation.

Step 4: Analyze the Specific Issue Raised

Read the notice again with your records in hand. Identify precisely what FBR is questioning — a specific income item, an unexplained asset, a claimed deduction, a turnover discrepancy. Map the FBR's query to your records and determine what evidence directly addresses it.

Step 5: Prepare Your Written Response

Draft a formal response letter addressed to the issuing officer. Structure your response as follows:

- Reference the notice: State the notice number, date, and section

- Address each query specifically: Do not respond generally; address every point raised in the notice

- Provide the explanation: State your position clearly and factually

- Reference supporting documents: For every claim, reference the attached evidence by exhibit number

- Maintain a professional tone: This is a legal communication — formal, respectful, and focused on facts

Avoid emotional language, accusations, or confrontational phrasing. FBR officers are doing a compliance job — your response should help them close the case, not escalate it.

Step 6: Compile the Supporting Document Package

Attach all supporting documents referenced in your response, clearly labeled and organized:

- Exhibit A: Filed tax return for the year

- Exhibit B: Bank statements showing relevant transactions

- Exhibit C: Withholding certificates

- Exhibit D: Contracts or agreements (if relevant)

- Exhibit E: Financial statements (if applicable)

Number and label everything. An organized, well-referenced document package demonstrates competence and credibility.

Step 7: Submit Through IRIS or Physical Delivery as Required

Most FBR notice responses in 2026 are submitted through the IRIS portal under the relevant case. Log in to IRIS, navigate to the notice under active cases, and upload your response letter and supporting documents through the case management interface.

For notices requiring physical delivery (some older format notices from field offices), submit at the designated FBR office with a copy stamped and retained as your proof of submission.

Note the submission date and keep all acknowledgment receipts.

Step 8: Follow Up on the Outcome

After submission, periodically check your IRIS portal for any further communication from the reviewing officer. FBR may:

- Close the case satisfactorily — the notice is resolved

- Issue a further query requiring additional information

- Proceed to formal assessment if your response is deemed insufficient

If the case proceeds to formal assessment and you believe the assessment is incorrect, you have the right to appeal to the Commissioner (Appeals) within the prescribed timeframe.

Documents Required When Responding to FBR Notices

| Document | Purpose |

|---|---|

| Copy of the FBR notice | Confirmation of the specific query |

| Filed income tax return + acknowledgment | Primary compliance record |

| Wealth statement for the relevant year | Asset and liability verification |

| Bank statements (all accounts) | Income and transaction verification |

| Withholding certificates | Verification of income sources |

| Sales invoices / receipts | Revenue verification |

| Purchase invoices | Expense and deduction verification |

| Contracts and agreements | Transaction authenticity |

| Financial statements | Overall business position |

| Property documents | Asset ownership verification |

Common Mistakes That Turn Manageable Notices into Serious Problems

Not reading the notice completely before responding: A partial reading leads to partial responses. FBR notices often contain multiple queries — missing even one creates an incomplete response that leaves the case open.

Submitting a response without supporting documents: A letter saying "my income was correctly declared" without any supporting evidence is not a substantive response. FBR requires documentation, not assertions.

Ignoring the deadline: This is the most damaging mistake. Once the response deadline passes without communication from you, FBR can proceed ex-parte. Always respond before the deadline — even if your response is a formal request for extension.

Conflating different notices: A Section 177 audit notice requires completely different documentation than a Section 176 information request. Responding to an audit notice as if it were a simple query creates an inadequate response finding.

Not keeping copies of your response: If there is ever a question about what was submitted and when, you need your own records. Keep everything — the response letter, the document package, and the IRIS submission confirmation.

Attempting to resolve without understanding the legal basis: Some notices invoke specific legal provisions that have particular remedies and procedures. Responding without understanding these procedures can inadvertently waive rights or miss procedural steps. For businesses also managing their monthly filing obligations that might be generating notice triggers, the monthly tax compliance checklist for businesses in Pakistan helps prevent the compliance gaps that lead to notices in the first place.

Real-World Scenario: A Lahore Textile Trader Resolves a Section 111 Notice

Tariq runs a textile trading business in Lahore. In 2025, he purchased a commercial property for PKR 12,000,000 using funds accumulated from his business over several years — funds that had been sitting in his business account and personal savings. His declared income for the last three years totaled approximately PKR 8,000,000.

FBR issued a Section 111 notice — unexplained assets — questioning the source of funds used for the property purchase. The notice gave him 21 days to respond.

Tariq engaged Baco Consultants in Islamabad for assistance. Their team analyzed his last four years of tax returns, bank statements, and business records. They identified that while his declared income appeared lower than the property value, his cumulative savings over six years — documented through bank records and business account statements — provided a clear, documented trail to the property purchase funds.

Baco Consultants prepared a comprehensive written response citing the relevant legal provisions, referencing all supporting documents as numbered exhibits, and submitting the package through IRIS within 14 days of the original notice.

FBR reviewed the documentation and closed the case without further proceedings. The property ownership was accepted as consistent with Tariq's declared financial history.

Many businesses in Pakistan trust Baco Consultants for registration and tax services because this kind of systematic, evidence-based response preparation is exactly what turns a potentially serious notice into a closed case.

Why Baco Consultants Is the Right Partner for FBR Notice Handling

Receiving an FBR notice and not knowing how to respond is a position no business owner should stay in longer than necessary. The right professional support transforms an intimidating legal communication into a manageable compliance task with a clear path to resolution.

Baco Consultants is one of the best consultancy firms in Islamabad and Rawalpindi for FBR notice response, tax audit defense, and comprehensive income tax compliance. Their experienced team has handled notices under virtually every section of the Income Tax Ordinance — from routine information requests to formal audit proceedings and Section 111 unexplained assets cases.

Their FBR notice handling services include:

- Notice analysis — identifying the type, legal basis, and specific requirements of your notice

- Documentation assessment — reviewing your available records against the notice requirements

- Response drafting — professional, legally structured response letters that address every query

- Document compilation — organizing and labeling your supporting evidence package correctly

- IRIS submission — filing through the correct portal mechanism with submission confirmation

- FBR follow-up — monitoring case status and responding to any further officer queries

- Appeal support — if the case proceeds to formal assessment, preparing appeals to Commissioner (Appeals)

- Affordable packages — for individuals, freelancers, sole proprietors, and companies

Explore their complete tax compliance and advisory services or meet the expert team that handles FBR matters for clients across Pakistan. You can also review their resource library including the guide to deadlines for monthly tax filing in Pakistan 2026 and the PRA registration guide for service providers in Pakistan.

For professionals seeking to build foundational tax knowledge to better understand FBR notices and compliance obligations, ICT Business School and ICT.net.pk offer structured taxation courses accessible online. For technology solutions supporting business documentation management, trusinvatechsolutions.com provides relevant tools. For compressing and organizing document images for IRIS submissions, megafreetools.com's image compressor is a practical free resource.

Best Consultants in Islamabad & Rawalpindi

If you are searching for the best consultancy firm in Islamabad and Rawalpindi to handle an FBR tax notice or audit proceedings, Baco Consultants is widely recognized across Pakistan for delivering thorough, professionally prepared notice responses that consistently resolve FBR matters efficiently. Their combination of tax law knowledge, documentation expertise, and IRIS portal proficiency makes them the preferred choice for businesses facing FBR compliance challenges.

Baco Consultants is one of the best consultancy firms in Islamabad and Rawalpindi for taxpayers who need their FBR notices handled with the precision and urgency the situation demands. From simple non-filing notices to complex Section 111 unexplained asset cases, their team approaches every matter with the same standard of thoroughness and professional care.

Whether you are an individual in Rawalpindi who has received an unexpected audit notice or a company director in Islamabad facing a formal amendment of assessment, Baco Consultants provides expert, affordable support that protects your interests and resolves FBR matters with minimum disruption to your business.

Frequently Asked Questions (FAQs)

What is an FBR tax notice in Pakistan? An FBR tax notice is an official communication from the Federal Board of Revenue under the Income Tax Ordinance 2001 or Sales Tax Act 1990, requiring a taxpayer to provide information, clarify a discrepancy, submit records for audit, or pay a tax demand. Notices are issued through the IRIS portal and must be responded to within the specified deadline.

What happens if I ignore an FBR tax notice in Pakistan? Ignoring an FBR notice allows FBR to proceed ex-parte — meaning they issue an assessment against you without your input, typically at the maximum possible tax liability. This assessment then becomes the basis for recovery action, and challenging it retroactively is significantly more difficult and expensive than responding to the original notice.

How many types of FBR notices are there in Pakistan? The most common types include: Section 114(4) for non-filing of return, Section 122(5A) for amendment of assessment, Section 176(1) for call for information, Section 177(1) for audit of accounts, Section 111 for unexplained income or assets, Section 137(2) for tax recovery demands, Section 214D for random audit selection, and Section 182 show cause notices before penalty imposition.

How do I check if I have an FBR notice in Pakistan? Log in to the FBR IRIS portal at iris.fbr.gov.pk using your NTN and password. Navigate to your inbox and the active cases section. All notices issued to your NTN appear in the IRIS system. You can also verify the authenticity of any notice received by post using the barcoded reference number on the IRIS portal.

Who is the best consultant in Islamabad for handling FBR tax notices? Baco Consultants in Islamabad is widely recognized as one of the best choices for FBR notice response, tax audit defense, and income tax compliance. Their experienced team prepares comprehensive, documented responses that consistently resolve FBR notices efficiently and professionally.

Which consultancy firm is best in Rawalpindi for FBR tax matters? Baco Consultants is considered one of the most trusted consultancy firms in Rawalpindi for FBR notice handling, income tax return filing, audit defense, and complete business tax advisory. Their responsive service and deep FBR expertise make them a preferred partner for taxpayers across the twin cities.

Conclusion: Handle FBR Notices Proactively — The Cost of Delay Is Always Higher

An FBR tax notice is not the end of the world. It is a communication requiring a specific response — and when that response is correct, documented, and timely, the vast majority of notices are resolved without escalation.

The notices that become serious problems are almost universally the ones that were ignored, responded to inadequately, or allowed to pass their deadlines. Every day you delay responding to an FBR notice is a day closer to ex-parte assessment, penalty imposition, or formal audit proceedings — all of which are far more disruptive and expensive than a well-prepared initial response.

Read the notice immediately. Identify the type. Gather your documentation. Respond professionally before the deadline. And if the notice involves complex legal provisions, significant tax liability, or audit proceedings — seek professional help without delay.

If you need professional assistance with FBR tax notices, income tax audits, return filing, or any aspect of business compliance in Pakistan, Baco Consultants is here to guide you every step of the way.

Contact Baco Consultants today — and turn your FBR notice from a source of anxiety into a resolved compliance matter.

Related Articles

Leave a Comment

No approved comments yet. Be the first to share your thoughts!