Your phone buzzes at 9 AM on a Tuesday. It is your accountant: "You have received an FBR notice. What do you want to do?"

That single sentence triggers a cascade of anxiety for most Pakistani taxpayers. Thoughts race — Is it an audit? Will I face penalties? Did I make an error in my last return? How much time do I have?

Here is the truth that most people do not hear often enough: receiving an FBR notice does not mean you have done something wrong. Many FBR notices are routine system-generated communications triggered by data mismatches, non-filing reminders, or random audit selection. What matters — far more than receiving the notice — is how you respond to it.

A correct, timely, and well-documented FBR notice response resolves the vast majority of cases without escalation. This guide gives you the complete FBR compliance roadmap for 2026.

What Is an FBR Notice Response in Pakistan?

An FBR notice response is a formal, documented reply submitted by a taxpayer — through the FBR IRIS portal or physically to the issuing tax office — addressing the specific query, discrepancy, or demand raised in an official communication from the Federal Board of Revenue.

Under the Income Tax Ordinance 2001 and Sales Tax Act 1990, FBR has legal authority to issue various types of notices to taxpayers requiring information, clarification, audit access, or payment of assessed tax. Each type of notice has a specific legal basis, response requirement, and deadline.

The response process involves three core elements: understanding what the notice is asking, assembling documented evidence that addresses the query, and communicating that evidence through the correct procedural channel within the specified timeframe.

A notice response is not an argument with FBR. It is a factual, documented submission that allows the reviewing officer to close the case based on evidence. The clearer, more complete, and better-organized your response — the faster the resolution.

Why Correct FBR Notice Response Matters More Than Ever in 2026

In 2026, FBR's digital infrastructure is more integrated than at any previous point in Pakistan's tax history. The IRIS system cross-references declared income against banking data, customs records, utility connections, vehicle registrations, property transactions, and third-party withholding statements automatically.

This means two things for Pakistani taxpayers:

First, more notices are being generated — because FBR's automated matching system is identifying discrepancies at scale that previously required manual investigation.

Second, the quality of your response matters more — because the same automated system tracks response submissions, monitors deadlines, and flags inadequate responses for further proceedings.

The consequences of handling FBR notices incorrectly in 2026 are significant:

Ex-parte assessment: If you do not respond, FBR issues a tax assessment against you without your input — typically at the maximum possible liability calculation. This assessment becomes the legal basis for recovery proceedings.

Penalty imposition: Non-response or inadequate response to certain notice types triggers mandatory penalty provisions under the Income Tax Ordinance, starting from fixed amounts and escalating with continued non-compliance.

Tax recovery action: Section 137 demand notices that are not addressed lead to direct recovery action — including bank account attachment, property attachment, and salary deduction orders.

Audit escalation: An inadequate response to an information request or audit notice can escalate a routine case into a full comprehensive audit covering multiple tax years.

ATL status impact: Extended non-compliance through unresolved FBR notices can affect your Active Taxpayer List status and create cascading banking and compliance complications.

The path away from all of these consequences runs through a single point: a timely, correct, documented response.

Types of FBR Notices You May Receive

Understanding which type of notice you have received determines the entire response strategy:

Section 114(4) — Non-Filing Notice: Issued when FBR's system shows you were required to file a return but did not. Response: file the outstanding return immediately.

Section 176(1) — Call for Information: FBR requests specific documents or data. Response: provide the requested information with supporting documents by the deadline.

Section 177(1) — Audit of Accounts: Your return has been selected for audit. Response: compile complete accounting records, financial statements, and all supporting documentation for the selected tax year.

Section 122(5A) — Amendment of Assessment: FBR proposes to change your filed assessment because they believe income was understated or deductions were overclaimed. Response: provide evidence supporting your original declaration.

Section 111 — Unexplained Income or Assets: FBR has identified assets or income that cannot be reconciled with your declared income history. Response: document the source of funds or assets through bank records, prior savings, loans, or inheritance documentation.

Section 137(2) — Recovery Demand: FBR demands payment of an assessed tax liability. Response: either pay the demanded amount or formally appeal the underlying assessment to Commissioner (Appeals).

Section 182 Show Cause Notice: Issued before FBR imposes a penalty, giving you the right to explain why the penalty is not warranted. Response: provide explanation with supporting evidence within the specified period.

Section 214D — Random Audit Notice: Your return was randomly selected for audit through FBR's computerized balloting system. Response: similar to Section 177 — compile full records for the selected year.

Key Requirements for an Effective FBR Notice Response

Before drafting your response, ensure you have these elements ready:

- Clear identification of the notice type and section — this determines what the response must contain

- Response deadline — typically 15 to 30 days from notice date; never allow this to pass without at least submitting an extension request

- Complete financial records for the relevant tax year — returns, bank statements, withholding certificates, invoices, financial statements

- A formal response letter — professionally structured, factual, and addressing every point raised

- Supporting document package — all evidence organized, labeled, and referenced in the response letter

- IRIS portal access — most responses are now submitted digitally through IRIS under the active case

Step-by-Step Guide: How to Respond to an FBR Notice in Pakistan 2026

Step 1: Read the Notice Carefully and Completely

This sounds obvious — but many taxpayers skim notices, miss critical details, and submit incomplete responses as a result. Read every line. Identify the issuing section, the specific issue raised, every document or information item requested, the response deadline, and the officer's contact details.

If the legal language is unclear, seek professional guidance before taking any other step.

Step 2: Verify the Notice Through IRIS

Log in to the FBR IRIS portal at iris.fbr.gov.pk. Navigate to your inbox and active cases section. Verify that the notice you received matches what is recorded in the IRIS system. Fraudulent notices occasionally circulate in Pakistan — always confirm through IRIS before responding.

Note your case reference number — this appears on all your submissions and communications.

Step 3: Assess Your Available Documentation

Pull together all financial records for the relevant tax year or period:

- Filed income tax return with acknowledgment receipt from IRIS

- Wealth statement for the year

- Bank statements for all accounts — personal and business

- Withholding tax certificates received from clients, employers, or banks

- Sales invoices issued to clients

- Purchase invoices received from suppliers

- Contracts, agreements, or letters relevant to the queried transactions

- Financial statements — profit and loss, balance sheet

- Property documents, vehicle registration papers (if referenced in the notice)

- Prior year returns (for wealth statement reconciliation)

The quality and completeness of your documentation directly determines the strength of your response.

Step 4: Request an Extension If Genuinely Needed

If collecting the required documentation will take longer than the notice deadline allows, submit a formal extension request through IRIS or in writing to the issuing officer before the deadline expires.

Important: extension requests must be submitted before the deadline, not after. FBR grants extensions on a case-by-case basis — a valid, professionally stated reason for needing additional time is typically accepted for first extensions.

Step 5: Draft Your Formal Response Letter

Structure your response letter as follows:

Opening: Reference the notice number, date, and the section under which it was issued. State that you are submitting your response within the prescribed time.

Body: Address each specific query or point raised in the notice separately and clearly. For each point, state your position factually and reference the supporting document (Exhibit A, Exhibit B, etc.) that proves your claim.

Closing: Confirm that all requested information has been provided and request the case be considered closed. Offer to provide any additional information if required.

Maintain a formal, professional, and factual tone throughout. This is a legal communication — not a personal appeal.

Step 6: Compile and Organize Your Supporting Documents

Label every supporting document as a numbered exhibit referenced in your response letter. Create a document index at the beginning of your package:

- Exhibit 1: Filed income tax return + acknowledgment receipt

- Exhibit 2: Wealth statement for the relevant year

- Exhibit 3: Bank statements (Account A — all months)

- Exhibit 4: Bank statements (Account B — all months)

- Exhibit 5: Withholding certificates from clients/employers

- Exhibit 6: Relevant contracts or agreements

- Exhibit 7: Financial statements

Organized, indexed documentation signals competence and credibility to the reviewing officer. It also demonstrates that you have nothing to hide.

Step 7: Submit Through the IRIS Portal

Log in to IRIS. Navigate to the relevant case under active cases. Upload your response letter and all supporting documents through the case management interface. Submit and immediately download your submission confirmation receipt.

For notices from FBR field offices requiring physical submission, deliver your complete package with a copy stamped and returned to you as proof of submission. Retain the stamped copy permanently.

Step 8: Follow Up on Case Status

After submission, check your IRIS inbox and active cases section regularly — at least every two weeks. FBR may issue further queries, request additional documents, or update the case status. Respond to any further communications promptly.

If the case results in a formal assessment you believe is incorrect, you have the right to file an appeal to the Commissioner (Appeals) within 30 days of the assessment order.

Documents Required for FBR Notice Reply: Quick Reference

| Document Type | Purpose in Response |

|---|---|

| Filed return + acknowledgment | Confirms compliance baseline |

| Wealth statement | Asset and liability verification |

| Bank statements (all accounts) | Income and transaction evidence |

| Withholding certificates | Income source verification |

| Sales invoices | Revenue declaration support |

| Purchase invoices | Expense and deduction evidence |

| Financial statements | Overall business position |

| Contracts and agreements | Transaction authenticity |

| Property documents | Asset ownership evidence |

| Prior year returns | Wealth statement reconciliation |

Common Mistakes That Turn Simple Notices Into Serious Problems

Ignoring the notice entirely: The single most costly mistake. Non-response allows FBR to proceed with ex-parte assessment at maximum liability. Always respond — even if only to request an extension.

Responding without supporting documents: A letter saying "my income was correctly declared" without any evidence is not a substantive response. FBR requires documentation — assertions alone are insufficient.

Missing the deadline without requesting an extension: Once the deadline passes without communication from you, FBR treats it as non-response. Always contact FBR before the deadline if you need more time.

Responding to the wrong notice type: A Section 177 audit notice requires full accounting records. Responding with a brief explanation letter misses the fundamental requirement of the notice type.

Not reading every point in the notice: Multi-point notices require responses to every point. A response that addresses three of four queries leaves the fourth unresolved — keeping the case open.

Not keeping copies of submissions: If FBR ever claims non-receipt or disputes what was submitted, you need your own records. Keep every response letter, document package, and IRIS submission confirmation permanently.

Not seeking professional help for complex notices: Section 111 unexplained income notices, Section 122 amendment proposals, and full audit notices involve legal procedures and documentation requirements that genuinely benefit from professional expertise. Attempting these without guidance risks missing critical procedural steps.

For businesses that want to prevent notices from arising in the first place, maintaining clean monthly compliance is the most effective strategy. The monthly tax compliance checklist for businesses in Pakistan helps businesses build the compliance systems that prevent the gaps FBR notices target. Understanding deadlines for monthly tax filing in Pakistan 2026 ensures you never miss the filing deadlines that generate automatic non-filing notices.

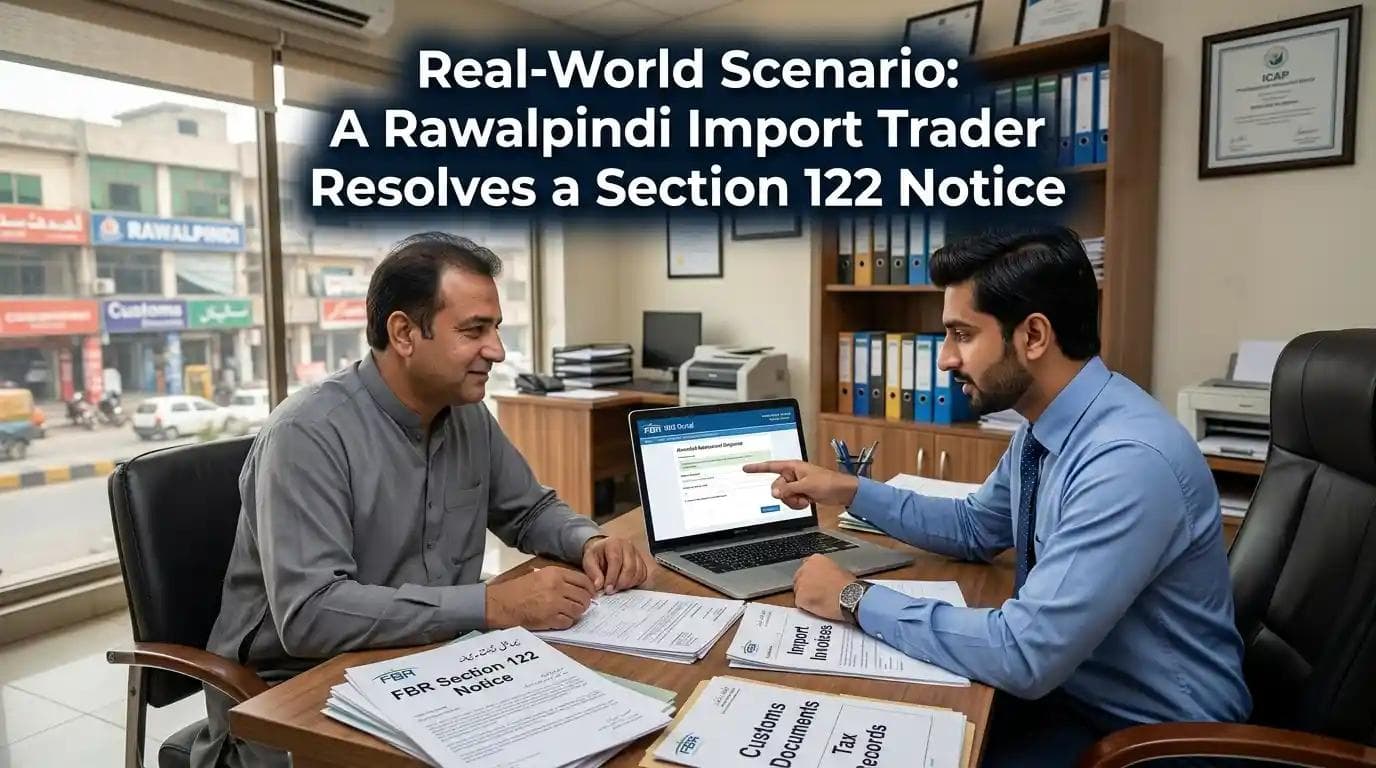

Real-World Scenario: A Rawalpindi Import Trader Resolves a Section 122 Notice

Zubair runs an import trading business in Rawalpindi. In his tax return for 2024, he claimed business expenses of PKR 4,200,000 against gross revenues of PKR 9,500,000 — resulting in net income of PKR 5,300,000. FBR issued a Section 122(5A) notice proposing to disallow PKR 1,800,000 of his claimed expenses, arguing they were not sufficiently documented.

The notice gave him 21 days to respond.

Zubair contacted Baco Consultants Rawalpindi immediately. Their tax team reviewed his expense records and identified that while the expenses were genuine, his documentation was incomplete — several supplier invoices were missing STRN details and three significant expense categories lacked supporting contracts.

Baco Consultants worked with Zubair over 10 days to gather supplementary documentation: supplier confirmation letters, payment receipts, bank transfer records for each expense item, and retrospective purchase documentation from suppliers who could provide it.

They drafted a formal Section 122(5A) response letter — professionally structured, addressing each disallowed expense category separately with the corresponding documentary evidence as numbered exhibits. The complete package was submitted through IRIS on day 16 of the notice period.

FBR reviewed the documentation and accepted PKR 1,550,000 of the originally disallowed expenses. A revised assessment was issued accepting net income of PKR 3,950,000 — significantly lower than the ex-parte assessment would have produced if Zubair had not responded.

Many businesses in Pakistan trust Baco Consultants for registration and tax services precisely because responses like Zubair's — systematic, evidence-based, and professionally structured — produce measurably better outcomes than unguided attempts.

Why Baco Consultants Is the Right Partner for FBR Notice Response

FBR notices are legal communications with legal consequences. The quality of your response directly determines the outcome. Professional guidance at this stage is not a luxury — for complex notices, it is the most cost-effective decision you can make.

Baco Consultants is one of the best consultancy firms in Islamabad and Rawalpindi for FBR notice response, tax audit management, and comprehensive income tax compliance. Their experienced team has handled notices under virtually every section of the Income Tax Ordinance — from routine information requests and non-filing notices to complex Section 111 unexplained asset cases and formal audit proceedings.

Their FBR notice handling services include:

- Notice analysis and classification — identifying the legal basis, specific requirements, and optimal response strategy

- Documentation assessment — reviewing your available records against notice requirements and identifying gaps

- Response letter drafting — professionally structured, legally sound, and addressing every query completely

- Document package compilation — organized, labeled, indexed, and referenced correctly

- IRIS portal submission — with submission confirmation and case monitoring

- Extension request management — filed before deadlines when additional time is genuinely needed

- FBR follow-up and query response — monitoring case status and addressing further officer requests

- Appeal preparation — if formal assessment proceeds, preparing Commissioner (Appeals) appeals within prescribed timelines

- Affordable packages — for individual taxpayers, sole proprietors, partnerships, and companies

Explore their complete tax compliance and advisory services and learn about their expert team before booking your consultation.

For businesses also managing provincial tax registrations alongside FBR compliance, the PRA registration guide for service providers in Pakistan and the Punjab sales tax filing guide for 2026 provide parallel compliance resources.

For foundational tax education that helps you understand the notices you receive, ICT Business School and ICT.net.pk offer structured taxation courses designed for Pakistani professionals. For document management tools supporting your IRIS submissions, trusinvatechsolutions.com provides useful technology resources, and megafreetools.com's image compressor helps optimize scanned documents for portal uploads.

Best Consultants in Islamabad & Rawalpindi

If you are looking for the best consultancy firm in Islamabad and Rawalpindi to handle an FBR notice professionally and protect your tax position, Baco Consultants is widely recognized across Pakistan for delivering thorough, evidence-based notice responses that consistently achieve favorable outcomes. Their systematic approach — notice analysis, documentation assessment, professional drafting, and IRIS submission — converts potentially serious compliance situations into resolved cases.

Baco Consultants is one of the best consultancy firms in Islamabad and Rawalpindi for taxpayers who need expert FBR guidance delivered quickly and affordably. Whether you are facing a routine non-filing notice, a Section 177 audit, or a complex Section 111 unexplained asset case, their team brings the same standard of professionalism and thoroughness to every matter.

From individual freelancers in Rawalpindi receiving their first FBR notice to established trading companies in Islamabad managing full audit proceedings, Baco Consultants provides the right expertise at the right time — making them the most trusted FBR notice consultants near me for businesses across the twin cities and beyond.

Frequently Asked Questions (FAQs)

How should I respond to an FBR notice in Pakistan? Read the notice completely to identify the type and specific requirements. Gather all relevant financial records. Draft a formal response letter addressing every point raised. Compile supporting documents as numbered exhibits. Submit through the FBR IRIS portal under the active case before the deadline. Keep confirmation receipts of everything submitted.

What happens if I ignore an FBR tax notice in Pakistan? Ignoring an FBR notice allows FBR to proceed ex-parte — issuing a tax assessment without your input at maximum possible liability. This assessment becomes the basis for recovery action including bank account attachment. Penalties for non-response also apply under the Income Tax Ordinance. Always respond before the deadline.

How many days do I have to reply to an FBR notice? Most FBR notices provide 15 to 30 days for response, depending on the notice type and the section under which it is issued. The specific deadline appears in the notice itself. If you need more time, submit a formal extension request through IRIS before the deadline expires — not after.

What documents are required to respond to an FBR notice? Core documents include your filed tax return with acknowledgment, wealth statement, bank statements for all accounts, withholding certificates, sales and purchase invoices, financial statements, and any contracts or agreements relevant to the queried transactions. The specific documents required depend on the notice type.

Who is the best consultant in Islamabad for FBR notice response? Baco Consultants in Islamabad is widely recognized as one of the best choices for FBR notice response, tax audit defense, and income tax compliance management. Their experienced team delivers professionally prepared, evidence-based responses that consistently resolve FBR matters efficiently.

Which consultancy firm is best in Rawalpindi for FBR tax matters? Baco Consultants is considered one of the most trusted consultancy firms in Rawalpindi for FBR notice handling, audit defense, income tax return filing, and complete business tax compliance. Many businesses and individuals across the twin cities rely on their expertise when FBR notices arrive.

Conclusion: Your Response Is Your Protection — File It Right

An FBR notice sitting unanswered in your IRIS inbox is not a problem that resolves itself. Every day without a response moves you closer to ex-parte assessment, penalty imposition, and potentially serious financial consequences.

The good news is straightforward: most FBR notices are resolvable when handled correctly. The right response — submitted on time, structured properly, and backed by solid documentation — closes the vast majority of cases without escalation.

Read every notice the day it arrives. Identify what type it is. Start gathering documentation immediately. Respond before the deadline. And for complex notices involving significant tax liability, audit proceedings, or unexplained asset queries — do not attempt to navigate the legal and procedural requirements alone.

If you need professional assistance with FBR notice response, income tax audit defense, return filing, or any aspect of business compliance in Pakistan, Baco Consultants is here to guide you every step of the way.

Contact Baco Consultants today and transform your FBR notice from a source of anxiety into a professionally resolved compliance matter.

Related Articles

Leave a Comment

No approved comments yet. Be the first to share your thoughts!